Do you want to buy antibiotics online without prescription? https://buyantibiotics24h.net/ - This is pharmacy online for you!

Opussamplehealthcare1.indd

Apricus Biosciences, Inc. Note | USA | Heath Care Sept-2011

Apricus Bio achieves another U.S. product approval! : DIPHENHYDRAMINE-D

NexMed USA, a wholly-owned subsidiary of Apricus Bio, received US marketing approval for

its over-the-counter (OTC) Diphenhydramine-D product. This approval follows on the heels of

two additional OTC products, Hydrocortisone-D (August 23, 2011) and Tolnaftate-D (August

18, 2011). We expect that these three products will be only a few of NexMed USA's OTC Consumer Healthcare Division's products.

Diphenhydramine-D treats itching and oozing/weeping of the skin caused by common skin ailments, such as insect bites, minor irritations and poison ivy. The active ingredients in this product are the topical analgesic, diphenhydramine hydrochloride and the skin protectorant, zinc acetate.

NexACT technology (DDAIP*) is utilized in Diphenhydramine-D to briefly loosen the tight

connections between skin cells. This action provides the product's active ingredients with

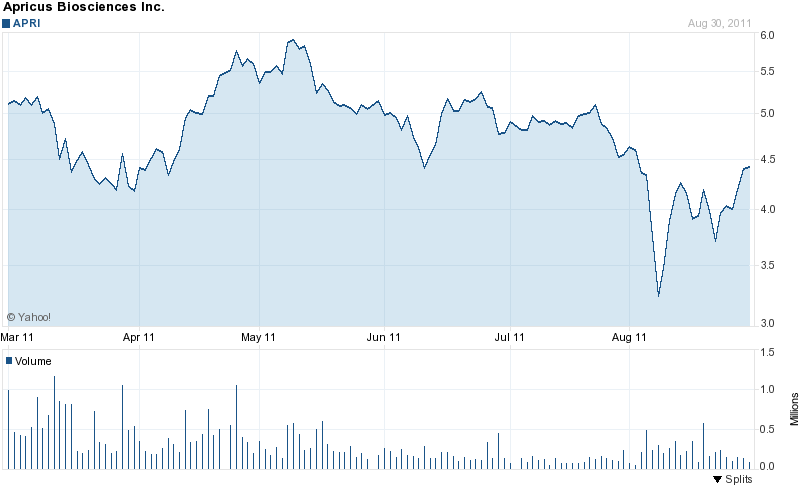

Stock Information

These three recent product approvals give us further confidence in Apricus Bio management's

capability to set and achieve corporate goals.

We continue to strongly believe that one of NexACT technology's main strengths is its potential

to extend the patent life of numerous drugs.

Diphenhydramine-D approval strengthens our belief in the monograph listing of Apricus Bio's

NexACT technology (DDAIP) as an excipient for approved OTC products. This listing should

be continually beneficial in paving the way for future approvals of NexACT combination

Until we have additional clarity on the launch of NexMed USA's OTC Consumer Healthcare

Division's product line, we are not adjusting our current estimates. This postponement in the

possible adjustment of our revenue expectations is not a reflection of our enthusiasm for this

corporate milestone and NexACT's future potential. We also remain focused on Apricus Bio's

abilities to increase revenues through partnering both its drug pipeline and the NexACT

technology. Specialty pharmaceutical companies, such as Depomed (Nasdaq. DEPO. Not

Rated), Antares(ASE.AIS.Not Rated) and BioSante (Nasdaq.BPAX.Not Rated) have stock

has a full pipeline that includes a topical

prices reflecting revenue multiples of 6-40X. Due to Apricus Bio progress during 2010-2011,

we believe that a 10X revenue multiple is appropriate. By using our 2013 revenue estimate, we

believe that Apricus Bio will have the appropriate time to meet its corporate goals, but we also

apply a 15% discount due to its evolving corporate

We maintain our coverage of Apricus Bio with a BUY recommendation and a price target of

$ millions 5,957,491 2,845,353 1,030,026 15,487,624 20,887,624 Operating income (5,173,854) (3,819,842) (21,400,977) (1,963,235) 6,281,035 Net Income (5,171,198) (32,042,562) (29,508,346) (1,963,235) 1,450,223

110 East Broward Blvd., Suite 1700 • Fort Lauderdale, FL 33301 • Office: 954.391.5305 • Fax: 646.417.7388 • www.OpusGroupFinancial.com

Page 1

Apricus Biosciences, Inc. Note | USA | Heath Care Sept-2011

MEANING OF RATINGS Buy We believe the company is undervalued relative to its market and peers. We believe its risk reward ratio strongly advocates purchase of the stock relative to other stocks in the marketplace. Remember, with all equities there is always downside risk. Speculative Buy We believe that the long run prospects of the company are positive. We believe its risk reward ratio advocates purchase of the stock. We feel the investment risk is higher than our typical “buy” recommendation. In the short run, the stock may be subject to high volatility and continue to trade at a discount to its market. Neutral We will remain neutral pending certain developments. Underperform We believe that the company may be fairly valued based on its current status. Upside potential is limited relative to investment risk. Sell We believe that the company is significantly overvalued based on its current status. The future of the company's operations may be questionable and there is an extreme level of investment risk relative to reward. Some notable Risks within the Microcap Market Stocks in the Microcap segment of the market have many risks that are not as prevalent in Large-cap, Blue Chips or even Small-cap stocks. Often it is these risks that cause Microcap stocks to trade at discounts to their peers. The most common of these risks is liquidity risk, which is typically caused by small trading floats and very low trading volume which can lead to large spreads and high volatility in stock price. In addition, Microcaps tend to have significant company specific risks that contribute to lower valuations. Investors need to be aware of the higher probability of financial default and higher degree of financial distress inherent in the microcap segment of the market.

110 East Broward Blvd., Suite 1700 • Fort Lauderdale, FL 33301 • Office: 954.391.5305 • Fax: 646.417.7388 • www.OpusGroupFinancial.com

Page 2

Apricus Biosciences, Inc. Note | USA | Heath Care Sept-2011

DISCLAIMER Opinions, information or ratings contained in this report are suggested solely for information purposes by qualified professional analysts. The opinions expressed in this research report are analyst’s personal views about the company. The information contained herein is based on sources which we believe to be reliable but is not guaranteed by us as being accurate and does not purport to be a complete statement or summary of the available data. Opus Group Financial, publisher, editor and their associates are not responsible for errors and omissions. Information on companies is provided sometime by the companies themselves, or is available from public sources or may be the opinion of the writer and Opus Group Financial makes no representations, warranties or guarantees as to the accuracy or completeness of the reported company. Any usage of the word “recommendation,” if any is to be defined as a “rating” only. The information may contains forward-looking information within the meaning of Section 27A of the Securities Act of 1993 and Section 21E of the Securities Exchange Act of 1934 including statements regarding expected continual growth of the company and the value of its securities. In accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 it is hereby noted that statements contained herein that look forward in time which include everything other than historical information, involve risk and uncertainties that may affect the company's actual results of operation. Factors that could cause actual results to differ include the size and growth of the market for the company's products, the company's ability to fund its capital requirements in the near term and in the long term, pricing pressures, unforeseen and/or unexpected circumstances in happenings, pricing pressures, etc. Investing in securities is speculative and carries risk. Past performance does not guarantee future results. Opus Group Financial or any of its affiliates may or not be registered investment advisors or registered with a FINRA member broker dealer. Opus Group Financial has been advised that the investments in researched companies are considered to be high risk and use of the information provided is at the investor’s sole discretion. Be advised that the purchase of such high risk securities may result in the loss of some or all of the investment. Investors should not rely solely on the information presented and or the opinion of others. Factual statements made in research and evaluation reports are made as of the date stated and are subject to change without notice. Investing in private, small and micro-cap securities is highly speculative and carries an extremely high degree of risk. It is possible that an investor’s entire investment may be lost or impaired due to the speculative nature of these companies. Opus Group Financial makes no recommendation that the securities of the companies researched and evaluated should be purchased, sold or held by individuals or entities that learn of the companies through Opus Group Financial. Opinions and recommendations contained in this report are submitted solely for advisory and information purposes and are not intended as an offering or a solicitation to buy or sell the securities. Readers are advised that this analysis report is issued solely for informational purposes. Neither the information presented nor any statement or expression of opinion, or any other matter herein, directly or indirectly constitutes a representation by the publisher nor a solicitation of the purchase or sale of any securities. The information used and statements of fact made have been obtained from sources considered reliable but neither guarantee nor representation is made as to the completeness or accuracy. No representation whatsoever is made by Opus Group Financial, its officers, associates or employees. Additional information on the company mentioned in this report is available upon request. It should be noted and made clear that this report should not be construed as advice designed to meet the particular investment needs of any investor. Such information and the opinions expressed are subject to change without notice. This report is not intended as an offering or a solicitation of an offer to buy or sell the securities mentioned or discussed. Opus Group Financial, it’s officers or employees may at any given time buy, sell, or trade these securities during the term of the contract. They may from time to time have a position in the securities mentioned herein and may increase or decrease such positions without notice. The analysts are strictly prohibited from buying, selling, or trading these securities during the term of the contract. Any opinions expressed are subject to change without notice. Opus Group Financial encourages readers and investors to supplement the information in these reports with independent research and other professional advice. Professional, credentialed analysts are paid fully in advance for their initial reports by Opus Group Financial to eliminate a pecuniary interest and insure independence. Opus certifies that no part of the analysts’ compensation was, is, or will be, directly or indirectly, related to the specific recommendation or views expressed by the analyst in the report. Analysts are under contract to Opus Group Financial to provide their reports solely for the benefit of the public. Opus Group Financial is under contract to be paid three thousand and five hundred dollars for an update research report and under agreement for monthly consulting and advisory services. The fees associated with this service are paid to Opus Group Financial and not directly to the analyst.

110 East Broward Blvd., Suite 1700 • Fort Lauderdale, FL 33301 • Office: 954.391.5305 • Fax: 646.417.7388 • www.OpusGroupFinancial.com

Page 3

Washout Periods for Brimonidine for latanoprost ( n ؍ 17) was 4.4 ؎ 3.2 weeks ( P ؍ .24). 0.2% and Latanoprost 0.005% In all but one patient, brimonidine returned to baseline by 5 weeks and latanoprost returned by 8 weeks. William C. Stewart, MD, Keri T. Holmes, and CONCLUSION: After discontinuing latanoprost or bri- Mark A. Johnson monidine, a wide variation exist

Larch and Echinacea Original Research Immunological Activity of Larch Arabinogalactan and Echinacea: A Preliminary, Randomized, Double-blind, Placebo-controlled Trial Linda S. Kim, ND, Robert F. Waters, PhD, and Peter M. Burkholder, MD Abstract complement properdin may be an indication OBJECTIVE: The immunomodulating effects of of one aspect of immune system stimulat

Apricus Biosciences, Inc. Note | USA | Heath Care Sept-2011

Apricus Bio achieves another U.S. product approval! : DIPHENHYDRAMINE-D

Apricus Biosciences, Inc. Note | USA | Heath Care Sept-2011

Apricus Bio achieves another U.S. product approval! : DIPHENHYDRAMINE-D  Apricus Biosciences, Inc. Note | USA | Heath Care Sept-2011

MEANING OF RATINGS

Apricus Biosciences, Inc. Note | USA | Heath Care Sept-2011

MEANING OF RATINGS  Apricus Biosciences, Inc. Note | USA | Heath Care Sept-2011

DISCLAIMER Opinions, information or ratings contained in this report are suggested solely for information purposes by qualified professional analysts. The opinions expressed in this research report are analyst’s personal views about the company. The information contained herein is based on sources which we believe to be reliable but is not guaranteed by us as being accurate and does not purport to be a complete statement or summary of the available data. Opus Group Financial, publisher, editor and their associates are not responsible for errors and omissions. Information on companies is provided sometime by the companies themselves, or is available from public sources or may be the opinion of the writer and Opus Group Financial makes no representations, warranties or guarantees as to the accuracy or completeness of the reported company. Any usage of the word “recommendation,” if any is to be defined as a “rating” only. The information may contains forward-looking information within the meaning of Section 27A of the Securities Act of 1993 and Section 21E of the Securities Exchange Act of 1934 including statements regarding expected continual growth of the company and the value of its securities. In accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 it is hereby noted that statements contained herein that look forward in time which include everything other than historical information, involve risk and uncertainties that may affect the company's actual results of operation. Factors that could cause actual results to differ include the size and growth of the market for the company's products, the company's ability to fund its capital requirements in the near term and in the long term, pricing pressures, unforeseen and/or unexpected circumstances in happenings, pricing pressures, etc. Investing in securities is speculative and carries risk. Past performance does not guarantee future results. Opus Group Financial or any of its affiliates may or not be registered investment advisors or registered with a FINRA member broker dealer. Opus Group Financial has been advised that the investments in researched companies are considered to be high risk and use of the information provided is at the investor’s sole discretion. Be advised that the purchase of such high risk securities may result in the loss of some or all of the investment. Investors should not rely solely on the information presented and or the opinion of others. Factual statements made in research and evaluation reports are made as of the date stated and are subject to change without notice. Investing in private, small and micro-cap securities is highly speculative and carries an extremely high degree of risk. It is possible that an investor’s entire investment may be lost or impaired due to the speculative nature of these companies. Opus Group Financial makes no recommendation that the securities of the companies researched and evaluated should be purchased, sold or held by individuals or entities that learn of the companies through Opus Group Financial. Opinions and recommendations contained in this report are submitted solely for advisory and information purposes and are not intended as an offering or a solicitation to buy or sell the securities. Readers are advised that this analysis report is issued solely for informational purposes. Neither the information presented nor any statement or expression of opinion, or any other matter herein, directly or indirectly constitutes a representation by the publisher nor a solicitation of the purchase or sale of any securities. The information used and statements of fact made have been obtained from sources considered reliable but neither guarantee nor representation is made as to the completeness or accuracy. No representation whatsoever is made by Opus Group Financial, its officers, associates or employees. Additional information on the company mentioned in this report is available upon request. It should be noted and made clear that this report should not be construed as advice designed to meet the particular investment needs of any investor. Such information and the opinions expressed are subject to change without notice. This report is not intended as an offering or a solicitation of an offer to buy or sell the securities mentioned or discussed. Opus Group Financial, it’s officers or employees may at any given time buy, sell, or trade these securities during the term of the contract. They may from time to time have a position in the securities mentioned herein and may increase or decrease such positions without notice. The analysts are strictly prohibited from buying, selling, or trading these securities during the term of the contract. Any opinions expressed are subject to change without notice. Opus Group Financial encourages readers and investors to supplement the information in these reports with independent research and other professional advice. Professional, credentialed analysts are paid fully in advance for their initial reports by Opus Group Financial to eliminate a pecuniary interest and insure independence. Opus certifies that no part of the analysts’ compensation was, is, or will be, directly or indirectly, related to the specific recommendation or views expressed by the analyst in the report. Analysts are under contract to Opus Group Financial to provide their reports solely for the benefit of the public. Opus Group Financial is under contract to be paid three thousand and five hundred dollars for an update research report and under agreement for monthly consulting and advisory services. The fees associated with this service are paid to Opus Group Financial and not directly to the analyst.

110 East Broward Blvd., Suite 1700 • Fort Lauderdale, FL 33301 • Office: 954.391.5305 • Fax: 646.417.7388 • www.OpusGroupFinancial.com

Page 3

Apricus Biosciences, Inc. Note | USA | Heath Care Sept-2011

DISCLAIMER Opinions, information or ratings contained in this report are suggested solely for information purposes by qualified professional analysts. The opinions expressed in this research report are analyst’s personal views about the company. The information contained herein is based on sources which we believe to be reliable but is not guaranteed by us as being accurate and does not purport to be a complete statement or summary of the available data. Opus Group Financial, publisher, editor and their associates are not responsible for errors and omissions. Information on companies is provided sometime by the companies themselves, or is available from public sources or may be the opinion of the writer and Opus Group Financial makes no representations, warranties or guarantees as to the accuracy or completeness of the reported company. Any usage of the word “recommendation,” if any is to be defined as a “rating” only. The information may contains forward-looking information within the meaning of Section 27A of the Securities Act of 1993 and Section 21E of the Securities Exchange Act of 1934 including statements regarding expected continual growth of the company and the value of its securities. In accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 it is hereby noted that statements contained herein that look forward in time which include everything other than historical information, involve risk and uncertainties that may affect the company's actual results of operation. Factors that could cause actual results to differ include the size and growth of the market for the company's products, the company's ability to fund its capital requirements in the near term and in the long term, pricing pressures, unforeseen and/or unexpected circumstances in happenings, pricing pressures, etc. Investing in securities is speculative and carries risk. Past performance does not guarantee future results. Opus Group Financial or any of its affiliates may or not be registered investment advisors or registered with a FINRA member broker dealer. Opus Group Financial has been advised that the investments in researched companies are considered to be high risk and use of the information provided is at the investor’s sole discretion. Be advised that the purchase of such high risk securities may result in the loss of some or all of the investment. Investors should not rely solely on the information presented and or the opinion of others. Factual statements made in research and evaluation reports are made as of the date stated and are subject to change without notice. Investing in private, small and micro-cap securities is highly speculative and carries an extremely high degree of risk. It is possible that an investor’s entire investment may be lost or impaired due to the speculative nature of these companies. Opus Group Financial makes no recommendation that the securities of the companies researched and evaluated should be purchased, sold or held by individuals or entities that learn of the companies through Opus Group Financial. Opinions and recommendations contained in this report are submitted solely for advisory and information purposes and are not intended as an offering or a solicitation to buy or sell the securities. Readers are advised that this analysis report is issued solely for informational purposes. Neither the information presented nor any statement or expression of opinion, or any other matter herein, directly or indirectly constitutes a representation by the publisher nor a solicitation of the purchase or sale of any securities. The information used and statements of fact made have been obtained from sources considered reliable but neither guarantee nor representation is made as to the completeness or accuracy. No representation whatsoever is made by Opus Group Financial, its officers, associates or employees. Additional information on the company mentioned in this report is available upon request. It should be noted and made clear that this report should not be construed as advice designed to meet the particular investment needs of any investor. Such information and the opinions expressed are subject to change without notice. This report is not intended as an offering or a solicitation of an offer to buy or sell the securities mentioned or discussed. Opus Group Financial, it’s officers or employees may at any given time buy, sell, or trade these securities during the term of the contract. They may from time to time have a position in the securities mentioned herein and may increase or decrease such positions without notice. The analysts are strictly prohibited from buying, selling, or trading these securities during the term of the contract. Any opinions expressed are subject to change without notice. Opus Group Financial encourages readers and investors to supplement the information in these reports with independent research and other professional advice. Professional, credentialed analysts are paid fully in advance for their initial reports by Opus Group Financial to eliminate a pecuniary interest and insure independence. Opus certifies that no part of the analysts’ compensation was, is, or will be, directly or indirectly, related to the specific recommendation or views expressed by the analyst in the report. Analysts are under contract to Opus Group Financial to provide their reports solely for the benefit of the public. Opus Group Financial is under contract to be paid three thousand and five hundred dollars for an update research report and under agreement for monthly consulting and advisory services. The fees associated with this service are paid to Opus Group Financial and not directly to the analyst.

110 East Broward Blvd., Suite 1700 • Fort Lauderdale, FL 33301 • Office: 954.391.5305 • Fax: 646.417.7388 • www.OpusGroupFinancial.com

Page 3